Renewables and technology are driving the recovery of sustainable investments

After a weak start to the year, sustainable investment (SI) indices recorded a sharp recovery in the second quarter of 2025, demonstrating resilience in a context of high volatility. Key sectors such as technology and the green economy led the rebound, with the Environmental Opportunities (EnvOps) indices standing out thanks to the growth of investments in renewable energy and energy efficiency . This dynamic confirms a global trend: investors are increasingly oriented towards solutions that combine financial returns and positive impact , in line with the objectives of decarbonization and ecological transition . This is what emerges from the July Sustainable Investment Insights – Quarterly Report published by FTSE Russell, a leading global provider of financial indices and analysis. This is a sign, the document states, that sustainable finance is not only resisting turbulence, but is establishing itself as a strategic lever for addressing future challenges. By integrating economic objectives with environmental, social, and governance (ESG) criteria, these strategies direct capital to companies capable of generating lasting value for investors, society, and the environment.

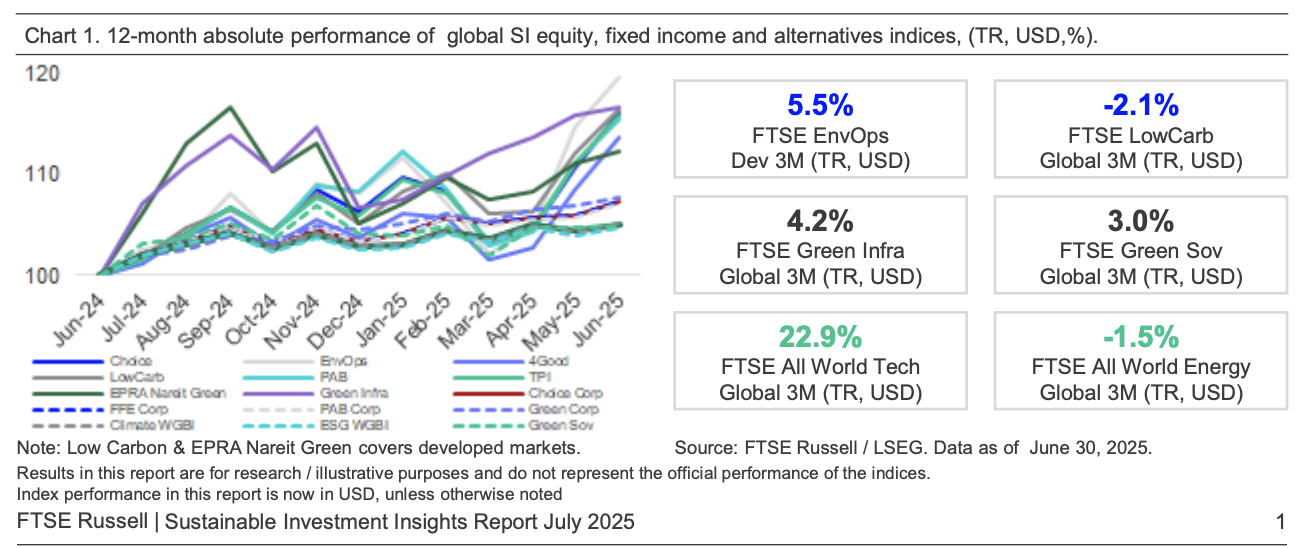

In the second quarter of 2025 , sustainable investment (SI) indices showed signs of recovery, despite market volatility. The technology sector , which had struggled in previous months, led the recovery with growth of nearly 23% , while the energy sector, previously the leader, lost 1.5% due to falling oil prices. The push towards a green economy reinforced this positive trend, with the Environmental Opportunities (EnvOps) indices supported by growing investments in renewable energy sources and energy efficiency.

Green bonds have performed well and increased issuance, with a strong presence of European securities. The sustainable infrastructure sector has also benefited from the revitalization of the railway sector, contributing to the overall strengthening of transition-related tools.

After the outflows of March and April, the following months saw greater stability in SI fund flows. However, attention remains high on geopolitical and macroeconomic dynamics, which continue to influence investor behavior.

The report highlights the diversity of SI strategies. Some indices, such as Global Choice , focus on eliminating fossil fuels and reducing carbon intensity. Others, such as FTSE4Good , favor companies with high ESG scores, while Environmental Opportunities selects companies with a strong green revenue stream. The Paris Aligned Benchmark and TPI Climate Transition indices pursue multiple objectives, including reducing emissions and strengthening climate governance.

Europe (excluding the UK) once again led the regional performance, supported by the euro's strengthening against the dollar . Despite tensions related to the tariffs announced on April 2 by the Trump administration, which caused a temporary decline in stock markets, their suspension a few days later and the start of negotiations between the United States and China fueled a climate of confidence, with a general return to risk-on for the rest of the quarter.

At a sector level, technology returned to the top, followed by cyclical sectors such as industrials, consumer discretionary, and financials, while healthcare and energy showed the weakest performances.

On the macroeconomic front, the International Monetary Fund (IMF) forecasts point to a slowdown in US growth in 2025-26 , compared to an expected recovery in developed markets starting in 2026. One- to three-year inflation expectations have fallen below 2% in most developed countries, while short-term expectations have increased in the United States , complicating the Federal Reserve 's decisions. Following the elections, rate cut forecasts in the US underwent one of the most marked reversals, making the country an anomaly compared to other advanced markets. Despite the outflows from bond funds recorded in April, global flows maintained a positive trend over the quarter.

The green economy shone thanks to the strong performance of the energy efficiency sector, driven by the recovery of industry and technology. Renewables also showed signs of growth, confirming a positive trend that reflects growing confidence in investments related to the ecological transition.

According to estimates by the International Energy Agency (IEA) , global investments in clean energy will reach $2.2 trillion by 2025, double that projected for fossil fuels. Solar remains a key player, with $450 billion in projected investments, while energy storage and electricity grids continue to grow, partly in response to critical events such as the blackout that hit Spain and Portugal.

Electric mobility is booming : 17 million electric vehicles were sold in 2024, accounting for 20% of new global registrations, with China leading the way ( 50% ), followed by EMEA ( 20% ) and the United States ( 10% ). This shift is reducing demand for oil and accentuating overcapacity in the fossil fuel market.

At the same time, interest in climate adaptation solutions is growing: 34% of medium-sized and large companies reported having taken such measures. The adaptation market is estimated to be worth around $1 trillion , with annual growth of 21% over the last four years.

The transition isn't just a matter of mitigation: it's increasingly clear that adapting to climate change will be as crucial as reducing its causes. And the market seems to be embracing this vision.

At the same time, the green bond market has shown vitality: issuance has increased, and the ratio of green bonds to total bonds has exceeded the five-year average. Performance has been strong both quarterly and annually, with Green Corp (green corporate bonds) leading the way thanks to the strong performance of the banking sector. Green Sov (green sovereign bonds) have also benefited from falling yields in Europe and the United Kingdom, although they remain penalized over the long term.

The European market continues to drive issuance, while in the United States, the presence of sovereign green bonds remains limited. Green Corp bonds show greater exposure to BBB-rated securities, offering higher yields but also a different risk profile than traditional bonds.

In summary, Q2 confirmed the growing role of green bonds in the global financial landscape, with signs of stability and investor interest. This is a sector worth keeping an eye on for those seeking opportunities related to the ecological transition.

In the second quarter of 2025, the Global Choice indices outperformed the global average, thanks to a targeted strategy that particularly benefited the United States and emerging markets . Overlap in the technology sector, underweighting in energy, and effective selection in financials supported results, while excessive exposure to healthcare and less effective selection in industrials held back performance in Europe , the United Kingdom , and Asia-Pacific .

Beyond their financial performance, these indices stand out for their ability to reduce carbon intensity , thanks to an approach that excludes or underweights high-emitting sectors such as energy, utilities, and basic materials. The only exception is the United Kingdom, where environmental effectiveness has been more limited.

The combination of sector selection and attention to ESG criteria confirms the role of Global Choice as a reference tool for those seeking sustainable investments with a balanced risk profile and less exposure to climate risks.

esgnews